Change your Financial Life in One Year

Get ready to take control of your financial destiny! This comprehensive planner is your one-stop-shop for mastering every aspect of your financial life. Whether you're just starting your career, cruising towards retirement, or navigating daily expenses, this planner has got you covered.

The Year Planner is designed to guide you through life's financial milestones with confidence. From setting foundations for success in your early career to optimizing investments and savings during your growth stage, and finally securing your golden years through retirement planning, this planner covers it all. Plus, it helps you manage daily expenses, budget, and cash flow.

Within its pages, you'll find expert insights on key financial concepts such as investment strategies, tax optimization, risk management, estate planning, and retirement income planning. Interactive tools, including budget builders, savings trackers, investment portfolio analyzers, retirement readiness assessments, and expense optimizers, will help you put theory into practice.

By using this planner, you'll clarify your financial goals and priorities, identify areas for improvement, develop a tailored financial plan, stay organized and on track, and ultimately achieve peace of mind. Whether you're a financial novice or a seasoned pro, this planner will refresh your knowledge, fill gaps in your understanding, provide actionable tips, and inspire financial confidence.

Embark on your journey to financial success today! The Year Planner will help you discover a clearer financial vision, increase savings and investments, reduce debt and stress, and secure a financial future that's bright and worry-free. So why wait? Dive in and start planning your path to financial freedom!

Empowering Your Financial Future, One Month at a Time

January

Payslip & Benefits | Your payslip is more than just a means to a living – it’s a gateway to securing your financial future.

By taking the time to review and comprehend your payslip, you can ensure that you're being paid correctly, that your taxes are in order, and that you're making the most of your employee benefits, such as pension or provident fund contributions.

Understanding your Payslip

Moreover, understanding your payslip can also help you identify areas where you can optimize your finances, such as reducing your tax liability or increasing your retirement savings. Visit the Understanding Your Payslip page.

Retirement Contributions

Your Retirement fund is a critical component of your overall financial plan, and it's vital to grasp how it operates, including how contributions are made, how funds are invested, and how benefits are paid out. By having a clear understanding of your retirement fund, you can make informed decisions about your retirement savings, such as choosing the right investment options, selecting the appropriate benefit structure, and ensuring that you're saving enough to meet your retirement goals. Visit the Provident & Retirement Fund page.

Beneficiary Nomination

By naming a beneficiary, you ensure that your retirement fund, life insurance policy, or other investments are paid out to the person or people you intend to benefit from them. Visit the Beneficiary Nomination page.

February

Investing & Growing your Money | Setting investment goals is just the first step toward securing your financial future.

By aligning your investment products with your goals, you can create a targeted strategy that maximizes returns, minimizes risk, and brings you closer to achieving your vision and create a harmonized investment plan that drives progress towards your financial aspirations. Visit the Investment Products & Asset Classes page.

Tax-Free Savings Account (TFSA)

TFSAs are an attractive option for saving for short-term goals, emergencies, or long-term investments, and can be used in conjunction with other savings vehicles, such as retirement annuities or unit trusts.

Exchange Traded Funds (ETFs)

ETFs allow investors to diversify their portfolios by pooling funds to invest in a variety of assets, such as shares, bonds, or commodities.

Unit Trusts

A unit trust is a type of investment fund that pools money from many investors to invest in a diversified portfolio of assets, such as shares, bonds, or property.

Notice Accounts

A Notice Account is a type of savings account that requires you to provide a specified period of notice, typically ranging from 30 to 90 days, before withdrawing your money. In exchange for this notice period.

March

Estate Planning | The process of managing and distributing your assets after death or incapacitation – is a crucial aspect of ensuring your legacy and protecting your loved ones.

By taking control of your estate plan, you can secure your future, safeguard your assets, and leave a lasting legacy for generations to come.

Estate Planning

By planning your estate, you can ensure that your legacy is protected, your loved ones are provided for, and your wishes are respected. Visit the Estate Planning page.

Funeral Cover vs Life Cover

Both covers offer peace of mind, financial security, and a safety net for your loved ones, allowing them to focus on grieving and healing rather than worrying about financial obligations, it is important to understand the distinct differences. Visit the Funeral Cover vs Life Cover page.

Group Life Cover

Knowing the details of your group life cover, such as the coverage amount, beneficiaries, and any exclusions or limitations, can help you ensure that you have adequate life insurance in place and that your loved ones are protected. Visit the Group Life Cover page.

Trusts

Trusts can also provide for the ongoing care and education of children, even if their parents are no longer alive. Furthermore, trusts can offer tax benefits and protection from creditors, ensuring that the assets are preserved for the benefit of the children. Visit the Trusts page.

April

Retirement Planning | Retirement is a milestone we all look forward to, but often don’t adequately prepare for.

We’ll explore how to harmonize your retirement aspirations with your retirement annuity, ensuring it works towards your vision. Additionally, we’ll delve into the world of provident fund contributions, explaining how they impact your retirement savings and what you can do to maximize their benefits. By understanding and optimizing these essential elements, you can achieve your retirement objectives and enjoy the freedom and security you deserve.

Provident & Retirement Fund

Increasing your provident fund contributions can have significant tax benefits.

Contributions to a provident fund are tax-deductible, which means that the amount you contribute reduces your taxable income. This can result in a lower tax liability and more money in your pocket.

By maximizing your provident fund contributions, you can make the most of these tax benefits and build a more secure retirement. Visit the Provident & Retirement Fund page.

Retirement Planning

Aligning your Retirement Annuity (RA) with your retirement goals is crucial to ensure a financially secure post-work life. A well-structured RA can help you achieve your desired retirement lifestyle by providing a steady income stream.

To align your RA with your goals, consider factors such as your desired retirement age, expected expenses, and income requirements. You should also review and adjust your RA contributions, investment portfolio, and benefit structure regularly to ensure they remain aligned with your changing needs and goals. Visit the Retirement Planning page.

May

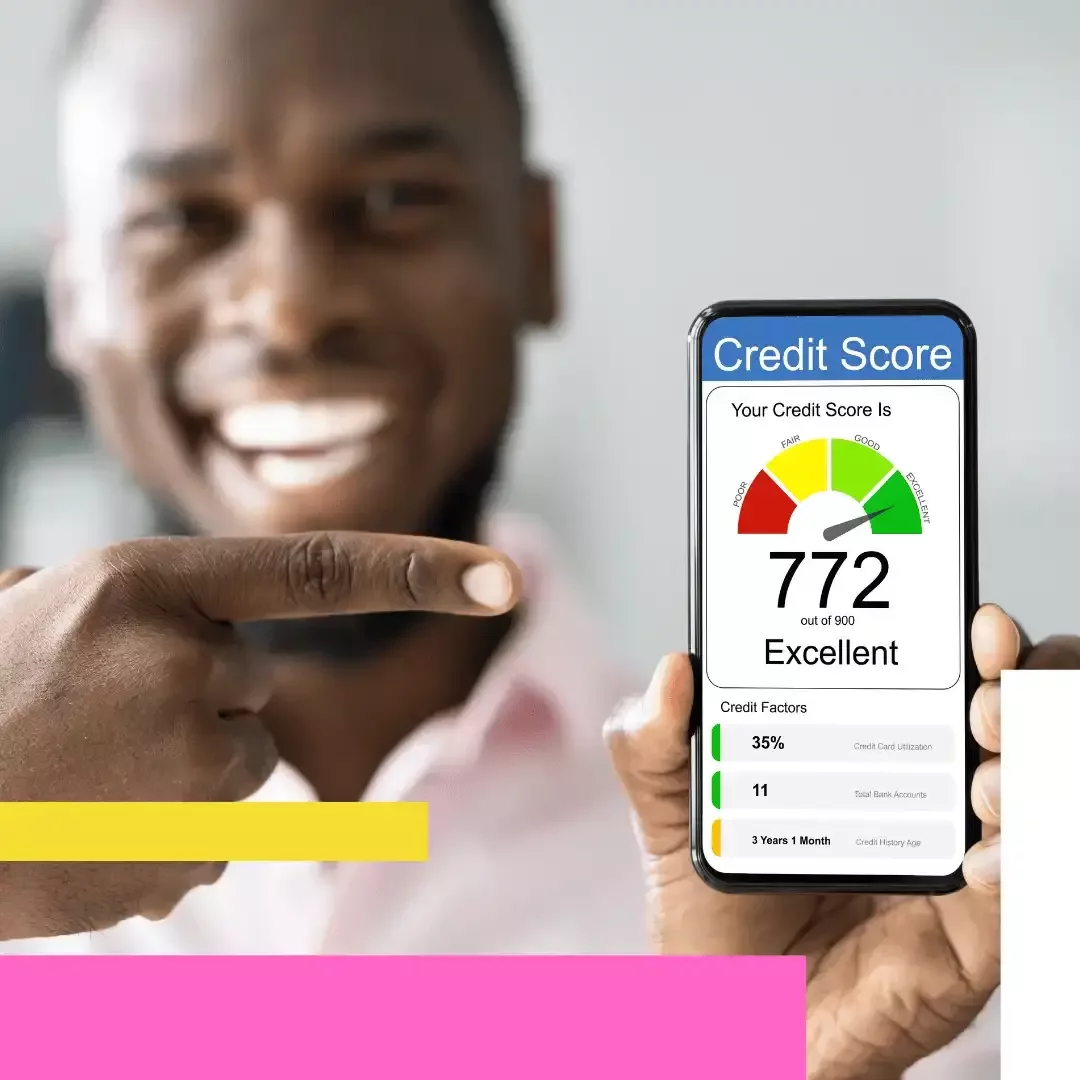

Credit Score vs Credit Report | Maintaining a good credit score and credit report is crucial for your financial well-being.

Credit Score vs Credit Report

A good credit score can help you qualify for loans and credit at favorable interest rates, while a poor score can lead to higher interest rates, loan rejections, and even impact your ability to rent a home or secure a job. Visit the Credit Report vs Credit Score page.

What you will need to do:

- Print Credit Report. Document each date & interest for each debt

- Document each date & interest for each debt

- Remove debit orders/ subscriptions you no longer use (i.e. gym membership)

Start Saving vs Paying Off Debt

When deciding whether to pay off debt or start saving, it's essential to strike a balance between the two. Find out what the best option is by visiting the Start Saving or Pay off Debt page.

What you will need to do:

- Print statements for all credit and loans. Document the interest for each debt

- Determine what method you will use to get rid off your debt

June

Tax | Understanding your tax obligations can have numerous benefits.

By being tax-savvy, you can minimize your tax liability, avoid penalties and fines, and maximize your refunds. Knowing how to navigate the tax system can also help you take advantage of tax incentives and deductions, such as medical expense credits, retirement annuity contributions, and home office expenses.

Additionally, understanding your tax obligations can help you make informed financial decisions, such as investing in tax-efficient products or structuring your income to minimize tax. Visit our Tax Season readiness page.

We’ll guide you on how to decode your tax obligations, identify potential savings, and avoid common pitfalls:

1) IRP5/IT3(a) employees Tax Certificate

2) Certificates received for:

– Local interest income

– Foreign interest income

– Foreign dividend income

3) The income tax certificate(s):

– Received for contributions made for Retirement annuities

3) Medical aid certificate

4) A logbook if you received a travelling allowance

5) Any other documents relating to income or deductions that were used in your

declaration of the return form

July

Insurance | Protection for your most valuable assets.

As your car depreciates over time, and your household circumstances change, your insurance coverage may no longer be optimized for your needs.

We’ll explore the importance of regularly updating your household, medical, and car insurance to ensure you’re not overpaying for coverage and provide tips on shopping for cheaper insurance options to save you money. By staying on top of your insurance coverage, you can avoid unnecessary costs, ensure adequate protection, and enjoy peace of mind knowing your assets are secure.

Having medical and general insurance is crucial for protecting yourself and your loved ones from financial ruin in the event of unexpected medical or insured events. Medical insurance, also known as medical aid, helps cover the high costs of private medical care, including hospitalization, surgery, and chronic medication.

General insurance, on the other hand, provides protection against losses or damages to your assets, such as your home, vehicle, and personal belongings.

By having both medical and general insurance, you can ensure that you are financially prepared for life's uncertainties, and avoid being burdened with unexpected expenses that could lead to financial hardship.

August

Crisis Management Plan | By being proactive and prepared, you can turn potential financial crises into manageable challenges and emerge stronger on the other side.

Life is unpredictable, and unexpected events can strike at any moment, threatening your financial stability.

Whether it’s a job loss, medical emergency, or unexpected disability, having a solid financial crisis management plan in place can be the difference between weathering the storm and financial ruin.

Financial Crisis Management Planning is not a task that can be put off until later. With the ever-changing economic landscape, unexpected financial shocks can occur at any moment, leaving you and your loved ones vulnerable. Creating a financial crisis plan immediately can help you prepare for the unexpected, ensuring that you have a safety net in place to weather financial storms. This plan should include building an emergency fund, reducing debt, diversifying investments, and identifying potential risk areas. By taking proactive steps to plan for a financial crisis, you can reduce stress, protect your assets, and ensure a more secure financial future.

We’ll provide practical tips and strategies for preparing for the unexpected, so you can safeguard your financial future and maintain peace of mind.

September

Will & Testament | Your Legacy is what makes everything you are doing worth it.

Having a Will & Testament in place is a crucial aspect of estate planning, ensuring that your assets are distributed according to your wishes and that your family is protected.

However, a Will is not a one-time task; it requires regular updates to reflect changing circumstances, such as new additions to the family, changes in assets, or shifts in personal relationships. We’ll explore the importance of having a will and keeping it updated, as well as the potential consequences of not having one in place.

We’ll delve into the complexities of intestacy laws, which govern the distribution of assets without a will, and examine the emotional and financial burdens placed on loved ones when there’s no clear plan. By understanding the significance of a will and keeping it current, you can ensure that your legacy is honoured, and your loved ones are cared for, even when you’re no longer present.

What you will need to do:

– Draft/Update a Will

– Print & Understand your Policy Schedule (Group Life etc)

October

Mental Health & Money Matters | Money matters can be a significant source of stress, anxiety, and emotional turmoil, impacting not only our financial well-being but also our mental health.

Our beliefs and feelings about finances can be deeply personal and often rooted in our past experiences, cultural background, and societal pressures.

However, when left unexamined, these beliefs can lead to unhealthy financial habits, self-sabotaging behaviors, and a perpetual cycle of financial stress. We’ll explore the intricate relationship between mental health and finances, highlighting the importance of acknowledging and addressing our emotional connections to money.

Join us as we shine a light on the critical intersection of mental health and financial well-being, and discover how awareness, self-reflection, and intentional habits can lead to a more balanced and fulfilling financial life. We will also be detailing the impact of Black Tax & Sandwich Generation and how to navigate it.

By examining our financial mindset and recognizing the impact of our beliefs on our financial decisions, we can begin to break free from limiting patterns and cultivate a healthier, more positive relationship with money.

Visit the Financial Emotions | Belief Systems & Anxiety page as well as the What is Your Money Personality page.

NOVEMBER

Silly Season Spending | With a little forethought and discipline, you can enjoy the festive season without breaking the bank or starting the new year with a financial hangover.

The December period, fondly known as the ‘Silly Season’, is a time of festive cheer, gift-giving, and indulgence. But with all the merriment comes a hefty price tag, and if you’re not careful, your finances can quickly spiral out of control.

During the Silly Season, which includes holidays like Christmas and New Year's, people often make common spending mistakes that can lead to financial regret. One of the biggest mistakes is overspending on gifts, decorations, and entertainment, often driven by emotions, social pressure, and a desire to create memorable experiences. Additionally, many individuals fail to budget for the Silly Season, leading to impulse purchases and dipping into savings or emergency funds.

Furthermore, the temptation to use credit cards or take out loans to finance holiday expenses can lead to debt and financial stress in the new year. By being mindful of these common spending mistakes, individuals can avoid financial pitfalls and enjoy a more sustainable and enjoyable Silly Season.

We will be preparing for the silly season

How much will you be spending over December?

Gift wealth

DECEMBER

Reflect & Plan | By examining our financial journey we can uncover trends, pinpoint unnecessary expenses, and make informed decisions about how to allocate our resources in the year ahead.

As the clock strikes midnight on New Year’s Eve, we’re not only bidding farewell to the old year but also to old habits and financial mistakes.

With this newfound understanding, you’ll be empowered to craft a budget that aligns with your values, supports your goals, and propels you towards a brighter financial future. Let’s dive in and make the most of this fresh start!

- Reflect and Plan for the following year

- Check the life stage planning model

- Plan on investing the additional money you will be saving in the new year with your improved spending habits!

Life Stage Planning

By creating a tailored financial plan, individuals can make informed decisions about saving, investing, and managing risk, ensuring that they are on track to meet their financial objectives. A financial life staging planning module also helps individuals anticipate and prepare for life's unexpected events, such as job loss, illness, or death, providing peace of mind and financial security.

By regularly reviewing and updating their financial plan, individuals can stay on course and achieve their long-term financial goals.