What do people typically invest for?

Retirement Savings: By investing in a retirement fund, you're building a safety net that will allow you to live comfortably, travel, and spend time with loved ones. It's about creating a future where you can focus on what truly matters. You can visit the Retirement Planning page to get helpful hints on how to calculate what you will need to retire comfortably

Wealth Creation: Wealth creation is about more than just accumulating riches – it's about building a better life for yourself and your loved ones. By investing in wealth-creating assets, you're taking control of your financial future and creating opportunities for growth, freedom, and security. How we view wealth is intricately part of who we are and how we were raised. Visit our Financial Emotions - Belief Systems and Anxiety

Education Expenses: Education is the key to unlocking a brighter future. By investing in education, you're giving yourself or your children the tools to succeed, grow, and thrive. It's about creating a legacy of knowledge, skills, and opportunities that will last a lifetime. Education builds the foundation for future growth and so does wealth. Learn more about setting up your lineage for financial success by visiting the Generational Wealth | Preparing for the Next Generation page.

Property & Home Upgrades: Down payment on a house, saving for a home purchase or upgrading to a new property - Home is where the heart is. By saving for a down payment, you're taking the first step towards owning your dream home, building equity, and creating a sense of stability and belonging. Whether you are purchasing property for the first time or planning on upgrading your current property, it is imperative to update your insurance. Find all the tips in our Insurance page.

Emergency Funds: Creating a Safety Net for Unexpected Expenses or Financial Setbacks. Life is unpredictable, and unexpected expenses can arise at any moment. By building an emergency fund, you're creating a financial safety net that will protect you from going into debt, reduce stress, and give you peace of mind. Don't get caught off-guard. Credit is not an Emergency Fund. Prepare yourself for the unexpected via our Crisis Management Planning page.

Income Generation: Financial freedom is about having the means to pursue your passions without worrying about money. While you let your money grow, take care of your current debt. Learn more about how to manage this by visiting the Start Saving or Pay Off Debt page.

Legacy Planning: Building Wealth to Leave a Lasting Legacy. What do you want to leave behind? By building wealth and creating a legacy plan, you're ensuring that your values, principles, and wealth are passed down to future generations, making a lasting impact on the world. We need to leave more than financial stability for our loved ones. Consider important documents and access to accounts when you are no longer there. We have an extensive list on our Legacy Locker page.

Major Purchases: Saving for Big-Ticket Items. Imagine being able to afford your dream car, wedding, or vacation without going into debt. By saving for major purchases, you're taking control of your financial future, avoiding debt, and creating memories that will last a lifetime. We need to develop smarter spending habits. Small changes allow us to have more money to invest. Reconsider your spending habits by simply checking out our Silly Season Spending page to see if you have spending habits you can improve on.

Personal Financial Goals: Achieving Specific Goals: What's your financial vision? By setting and achieving personal financial goals, you're taking control of your financial future, building confidence, and creating a sense of accomplishment and pride. Whether it's paying off debt, improving credit scores, or building an investment portfolio, you're investing in yourself and your financial well-being. Part of your financial wellness goals should include your Credit Health. The Improving Credit Health Status page will have everything you need to flex your financial muscles.

Business Investments: Funding Business Ventures, Expansions, or Entrepreneurial Endeavors. Are you an entrepreneur at heart? By investing in business ventures, you're taking calculated risks, pursuing your passions, and creating opportunities for growth, innovation, and success. Being smart about business also means being smart about WHO you leave your business to! Don't forget to visit the Will & Testament page and make sure yours is updated!

Following the 2008 meltdown of global credit and stock markets and the ensuing recession economic times are tougher. Workers today are faced with higher living expenses, falling house prices, prospects of retrenchments and decimated retirement savings balances. The days of people working in the same job for 30 years and then retiring to a nice fat pension are gone, the responsibility of planning for retirement has shifted to individuals. By planning ahead you can ensure financial stability, especially during retirement.

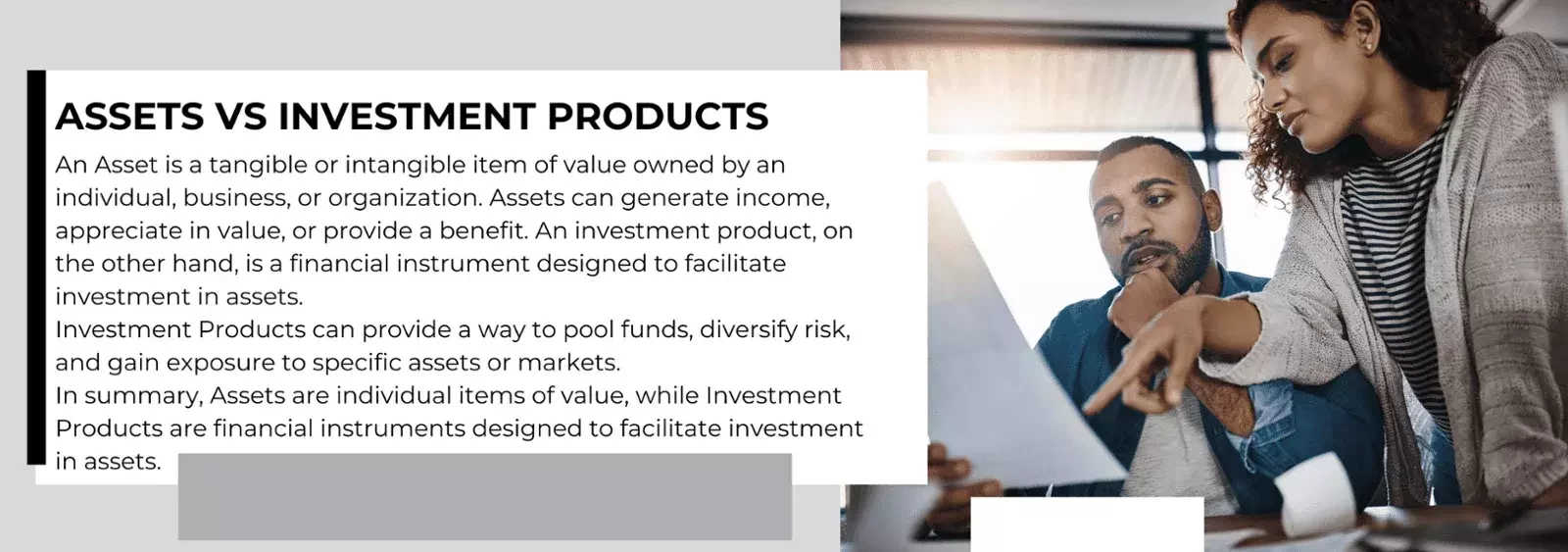

Understanding the distinction between an investment product and an asset class is a fundamental starting point in financial education. Many people use these terms interchangeably, yet they describe two very different layers of the investment world. Knowing how they differ helps individuals and businesses make informed decisions, diversify effectively and select financial tools that align with long term goals.

An asset class refers to a broad category of investments that share similar characteristics and behave in similar ways in the market. Examples include equities, fixed income, property, cash and commodities. Each asset class responds differently to market conditions and carries its own level of risk, return potential and volatility. Asset classes form the foundation of a diversified portfolio because they provide structure around how capital is allocated.

An investment product is a specific financial instrument that exists within an asset class. It is the actual vehicle an investor uses to gain exposure to that category. For example, within the equity asset class you may find individual shares, exchange traded funds and unit trusts. Within fixed income, you may find government bonds, corporate bonds and income funds. Products differ in structure, cost, accessibility and the level of expertise required from the investor. They are the practical tools used to implement an investment strategy.

Recognising the difference between these two concepts empowers investors to navigate the financial landscape with greater clarity. Asset classes help determine the overall direction and risk profile of a portfolio, while investment products provide the means to execute that strategy in a way that suits the investor’s needs and circumstances.

- Ownership: When you invest in an asset, you directly own that asset. In contrast, when you invest in an investment product, you own a share of the product, which in turn invests in assets.

- Structure: Assets are individual items of value, while investment products are financial instruments designed to facilitate investment in assets.

- Diversification: Investment products often provide diversification benefits by pooling funds and investing in a range of assets.

- Management: Assets are typically self-managed, while investment products are often managed by professionals, such as fund managers or investment advisors.

- Regulation: Investment products are subject to regulatory oversight, while assets themselves may not be.

Asset Classes

Investment characteristics: Such as the type of asset, its liquidity, and its risk profile.

Return expectations: Asset classes are often associated with specific return expectations, such as high returns for stocks or lower returns for bonds.

Risk profile: Asset classes have distinct risk profiles, such as market risk, credit risk, or liquidity risk.

Liquidity: Asset classes vary in their liquidity, with some assets being easily convertible to cash and others being less liquid.

Regulatory environment: Asset classes may be subject to different regulatory requirements, such as tax laws or securities regulations.

The key is finding a balance between the amount of risk you are willing to take and the potential returns you want to achieve. Each asset class has its own risk and return characteristics. The graph below shows the likely investment risk and growth prospects that can be expected from each asset class over the long term.

By spreading your investment among different asset classes, you can reduce the overall level of risk in your portfolio.

Investing Mindset

When considering investments, it's essential to define your goals: Are you seeking capital growth, aiming to supplement your income, or planning for retirement? Perhaps you're saving for large future purchases, such as a home or education expenses. Clarifying your objectives will help determine the most suitable investment strategy for your needs.

Determine your desired returns. Do you aim to earn additional income, surpassing your savings account's interest rate? Or, do you prioritize protecting your capital, even with modest returns? Perhaps you seek a long-term income stream, reasonable returns with capital growth, or high capital growth. Defining your return expectations will help guide your investment decisions.

Consider your time horizon. Will you need to access your savings soon for unexpected expenses, or can you afford to lock them away for an extended period? Your investment timeframe plays a crucial role in determining your risk tolerance and choosing the most suitable investment type.

When assessing risk, consider your personal factors: age, investment style, and emotional response to market fluctuations. Ask yourself: do you panic during downturns or remain confident in long-term returns? Are you willing to risk potential losses or do you prioritize stable, low-volatility returns? Understanding your risk tolerance will help guide your investment decisions.

Annuities | Endowment Policies:

An Endowment / Annuity is a contract between an investor and usually an insurance company that guarantees to compensate you as the investor a specific amount of money, periodically, for a particular period of time. As an example if you choose to take the annuity payments over your lifetime you will have a guaranteed source of “income” until your death.

The two primary reasons to use an annuity as an investment vehicle are:

– You want to save money for a long-range goal, and/or

– You want a guaranteed stream of income for a certain period of time.

Annuities lend themselves particularly well to funding retirement.

The earnings that occur during the term of the annuity are tax-deferred. You are not taxed on them until they are paid out. Since they are long-term investments and planning instruments, most of the annuities come with rules that may penalize the investor if they distribute or access the funds prior to reaching the established term.

The two primary reasons to use an annuity as an investment vehicle are:

– You want to save money for a long-range goal, and/or

– You want a guaranteed stream of income for a certain period of time.

Annuities lend themselves particularly well to funding retirement.

The earnings that occur during the term of the annuity are tax-deferred. You are not taxed on them until they are paid out. Since they are long-term investments and planning instruments, most of the annuities come with rules that may penalize the investor if they distribute or access the funds prior to reaching the established term.

Unit Trusts

Unit trust funds give you the option to withdraw money or put in extra when you want to. These funds give you the ability to invest in any asset class (i.e. equities, cash, bonds or property) or an asset sub-class (i.e. resources shares or financial shares) and various mixtures of asset classes called balanced funds. Your choice is extremely wide – currently there are nearly 800 funds in South Africa available to individual investors.

Returns from these funds try to mimic the underlying shares therefore are subject to fluctuations of the markets and returns can vary widely. You can consider past performance when assessing a fund, but this is no indicator of future performance.

In the unit trust universe actively managed funds, these are funds in which fund managers move in and out of assets to take advantage of market conditions, generally have higher asset management fees and often also charge performance fees. All funds publish a total expense ratio (TER), which represents the annual management costs, administration costs and various other fees, including bank charges and taxes as a percentage of your investment. The TER can range from less than one percent to more than three percent. It does not include the initial investment fee that unit trust companies often charge, nor does it cover the commission or fee that goes to your financial adviser, if you are using one.

Unit Trusts

Unit trust funds give you the option to withdraw money or put in extra when you want to. These funds give you the ability to invest in any asset class (i.e. equities, cash, bonds or property) or an asset sub-class (i.e. resources shares or financial shares) and various mixtures of asset classes called balanced funds. Your choice is extremely wide – currently there are nearly 800 funds in South Africa available to individual investors.

Returns from these funds try to mimic the underlying shares therefore are subject to fluctuations of the markets and returns can vary widely. You can consider past performance when assessing a fund, but this is no indicator of future performance.

In the unit trust universe actively managed funds, these are funds in which fund managers move in and out of assets to take advantage of market conditions, generally have higher asset management fees and often also charge performance fees. All funds publish a total expense ratio (TER), which represents the annual management costs, administration costs and various other fees, including bank charges and taxes as a percentage of your investment. The TER can range from less than one percent to more than three percent. It does not include the initial investment fee that unit trust companies often charge, nor does it cover the commission or fee that goes to your financial adviser, if you are using one.

ETFs | Exchange Traded Funds

Notice Accounts

A notice account is a type of savings account offered by banks and financial institutions in South Africa. It's a flexible savings product that allows you to earn interest on your deposits while still having access to your money.

Roles & Permissions

Trustees

Trustees are responsible for overseeing retirement funds or investment schemes on behalf of members or beneficiaries. Their primary duty is to act in the best interests of those members. This includes setting the fund’s investment strategy, ensuring proper governance, and monitoring performance and risks.

Advisors

Advisors work directly with individuals to help them make informed financial decisions. Their role is to understand a client’s goals, risk tolerance, time horizon, and financial situation, and then recommend suitable products and strategies.

For example, an advisor may help a client determine how much to save each month to achieve a target Net Replacement Ratio. They may also recommend specific investment products, review progress regularly, and adjust the plan as circumstances change. Advisors play a key role in translating complex financial concepts into practical, personalised action steps.

Asset Managers

Asset managers are professionals or firms responsible for making the actual investment decisions within a portfolio. They manage money on behalf of investors according to a specific mandate or strategy provided by the trustees or the investment product.

For example, an asset manager may be tasked with growing a retirement fund’s equity portion. They will research markets, select shares, bonds, or other assets, and adjust the portfolio over time to maximise returns while managing risk. Their performance directly impacts the growth of the investment and ultimately the retirement outcomes of the members.

Net Replacement Ratio (NRR)

The Net Replacement Ratio is a way of measuring how much of your income you will be able to replace when you retire. It compares your expected retirement income after tax to your final working income after tax, expressed as a percentage. This helps you understand whether your savings and investments will be enough to maintain your lifestyle once you stop earning a salary.

For example, if you earn 40,000 per month before retirement and your expected retirement income is 28,000 per month, your Net Replacement Ratio would be 70 percent. A ratio of around 70 to 80 percent is often considered a reasonable target, depending on your lifestyle and expenses. If your ratio is too low, it signals that you may need to increase your savings, adjust your investment strategy, or delay retirement. If it is higher than expected, it may indicate strong planning, but it is still important to consider factors like inflation, healthcare costs, and longevity.

Here is a simple, practical way to work out a Net Replacement Ratio step by step:

Step 1: Determine your final net income (after tax)

Assume you earn 50,000 per month before retirement. After tax and deductions, your take home pay is 40,000 per month.

Step 2: Estimate your retirement income (after tax)

Based on your savings, pension, or investments, you expect to receive 30,000 per month after tax in retirement.

Step 3: Apply the formula

![]()

Step 4: Calculate

NRR = (30,000 ÷ 40,000) × 100

NRR = 75 percent

What this means

You will replace 75 percent of your working income in retirement. If your expenses drop after retirement, for example no commuting or debt repayments, this may be sufficient. If your expenses stay the same or increase, you may need to boost your savings or adjust your plan to reach a higher ratio.

ETFSA | The Home of Exchange

Where you invest today could be one of the single biggest decisions you make in your life. That’s why it’s important that you understand – and are comfortable with – exactly where your money is going.

At ETFSA, we’ll help you embrace the power of Exchange Traded Funds and Products (ETPs), so you can access stock markets efficiently and securely. Whether you’re doing it yourself through our online platform or getting personalised advice from us in a bespoke ETF portfolio, we’ll help you build your wealth, your way.

Tax Free Investments | South Africa

The tax free investments may only be provided by a licensed bank, long-term insurers, a manager of registered collective schemes (with certain exceptions), the National Government, a mutual bank a co-operative bank, the South African Postbank, an administrative financial services provider and a person authorised by a licensed exchange to perform one or more securities services in terms of the exchange rules. Service providers must be designated by the Minister in the Gazette.